_1681884252.webp)

Table of Content

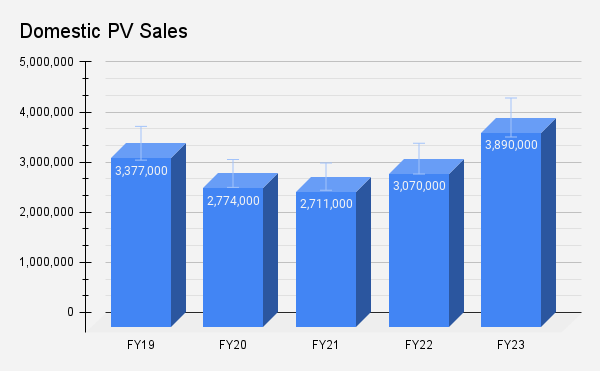

▼NEW DELHI: Owing to post-COVID pent up demand, easing of supply chain shortages, increased demand for SUV-style vehicles, and new product launches, Passenger Vehicles (PVs) posted their highest sales during 2022-23 at 38.9 lakh units, growing at a CAGR of 3.6% and surpassing the previous peak of 33.7 lakh in 2018-19.

Now, SUV-style vehicles make up 43% of the total PV market in India.

According to Vinod Aggarwal, President of the Indian Motor Manufacturers Association (SIAM), "2022-23 was a year of consolidation, post-Covid. The year started again with supply chain disruptions from the conflict in Ukraine. However, with effective management of supply chains and better availability of commodities. Especially for electronic goods, prices have softened over the course of the year, although it remains a concern.

Rohan Kanwar Gupta, Vice President and Sector Head- Corporate Ratings ICRA Ltd, says: "Industry retail sales were flat supported by healthy underlying demand. After some moderation in February 2023, flat demand along with the pre-purchase range prior to Phase II implementation of Baseline BS-VI issuances as of April 1, 2023 serve as a tailwind for March 2023 demand. With the help of these factors, volumes in the industry reached an all-time high of approximately 3.9 nm units in fiscal year 2023.”

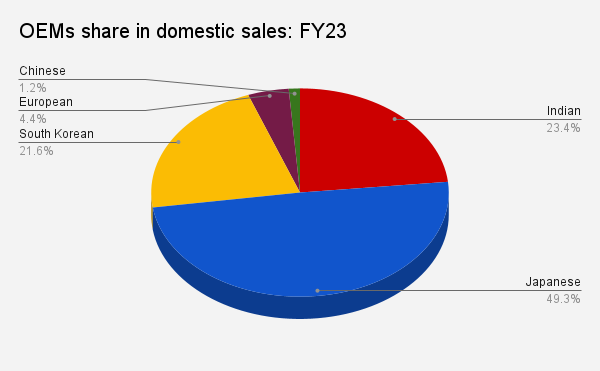

Indian OEM share nears 25%, Japanese dips below 50%

According to the latest data released by SIAM, the top three automakers Maruti Suzuki, Hyundai and Tata Motors reported their best sales performance for the fiscal year ending March 2023. Interestingly, the share of Indian automakers (Tata Motors, Mahindra and Mahindra) came close to addition to take up about a quarter of industry sales, while Japanese OEMs (Maruti Suzuki, Toyota, Honda, Nissan) dipped blow 50%.

During the 2021-22 fiscal year, Indian OEMs grabbed about 20% of the market share against the Japanese at 52%.

South Korean OEMs (Hyundai, Kia) continued to maintain their share at just over 21%.

Market leaders Maruti and Hyundai lose out; Tata, Mahindra, Kia gain

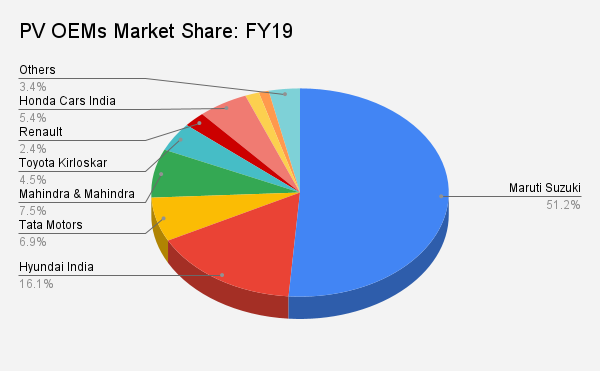

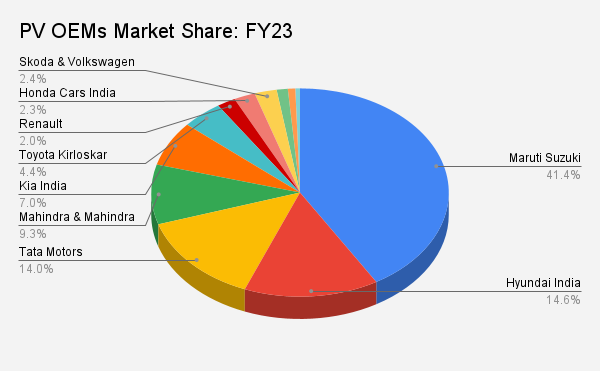

The country's largest carmaker, Maruti Suzuki, which used to grab more than half of the Indian domestic car market, has seen its share fall by 10% in just three years. The company that managed to maintain its 51% stake through 2019-20 fell to 48% the following year, followed by 44% in 2021-22 and finally 41% during the year ending March 2023. that new players like Kia and MG entered the Indian market in 2019-20.

However, the Japanese carmaker recently entered the midsize SUV segment with the Grand Vitara and also introduced its new Fronx and Jimny. With this, it aims to be the best seller in the SUV segment and expects to increase its overall market share to 45% in 2023-24.

Hyundai, which held its second position for the fiscal year, fell closer to Tata Motors. The Creta was only about 30,000 units ahead of the latter. Its market share is at its lowest level in the last five years with 14.5%. In 2020-2021, this is 17.4%. However, the company is betting on new feature- and technology-rich products for 2023-24.

On the other hand, the manufacturer Nexon more than doubled its share from 6.8% in 2018-2019 to 13.9% during the year ending March 2023. This is due to its portfolio of electric vehicles and the rebound in SUV style vehicles.

Mahindra & Mahindra is also revving up its market share with the demand for its new models including the Scorpio, XUV700 and Thar. Its share of the domestic market has hovered around 7% in the last four years and is now up to more than 9% in 2022-23.

South Korean automaker Kia, which marked its entry into the Indian market in 2019, occupies around 7% share of the domestic auto industry. In 1998, when sister company Hyundai entered the Indian market, it too managed to become a household name by acquiring a 10% stake in its first two years of operations.

Honda, which had more than 5% share of the Indian market in 2018-19, has dropped to around 2% by 2022-23. However, the company is all set to enter the best-selling SUV market in India this year. Last year, it also introduced the hybrid version of its flagship city sedan.

Nissan, which occupies less than 1% of the market, halted the production and sale of Datsun-brand cars in India during April 2022, after reviving it in the country in 2013.

Current challenges

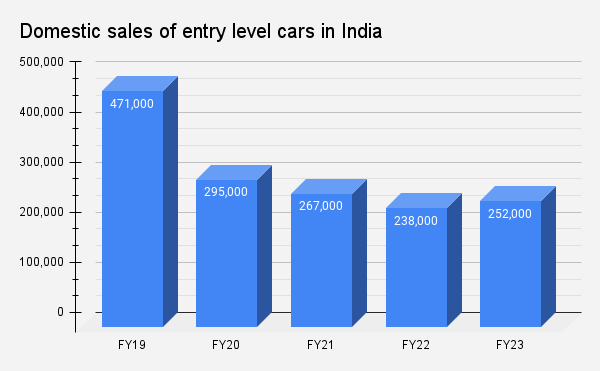

Due to changing consumer demand trends, new regulatory standards, and the rising cost of owning a vehicle, entry-level segment sales continue to decline. Compared to 2016-17, when sales in this segment were 5.83 lakh units, small car sales decreased by 57% to 2.52 lakh units.

Maruti, which pioneered small car sales, discontinued the Alto 800 hatchback this year.

Earlier, Hyundai also realigned its business strategy to focus on SUVs and sedans by pulling the plug on the once-popular Santro.

Although supply chain disruptions have improved, semiconductor shortages have not completely disappeared. Automakers expect that to continue for some time.

Exports

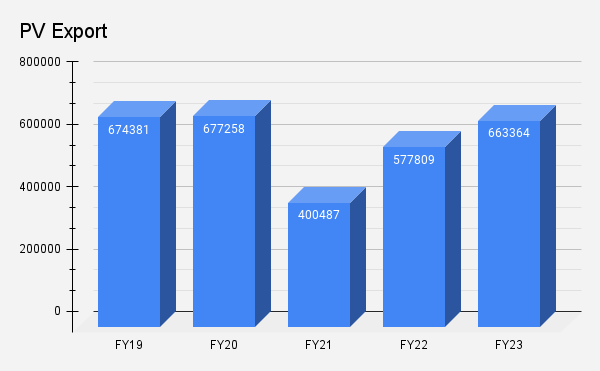

The country's passenger car exports grew in 2022-23 to surpass the 65 lakh mark three years later. Maruti Suzuki, the market leader in the domestic segment, has also acquired the number one position in the export of automobiles from India. The company which exported 2.55 lakh vehicles in 2022-23 ships to almost 100 countries. Africa, Latin America, Asia and the Middle East are important markets.

Other major PV exporters in the country include Hyundai which shipped 1.53 lakh units, Kia with 85,000 units and Nissan with more than 60,000 units.

However, the industry's exports during the year 2022-23 were still lower than in 2016-17 when it was 7.59 lakh units.

Outlook

To keep up with last year's high base, experts project healthy single-digit growth for 2023-24.

Rohan Kanwar Gupta, Vice President and Head of Sector - Corporate Ratings, ICRA Limited says: "Going forward, healthy replacement demand, new model launches and the availability of sufficient financing are likely to help the size of the industry grow between 6% and 9% in fiscal year 2024. However, the increase in the cost of ownership (driven by higher vehicle prices and repurchase rates) remains a significant obstacle for the industry”.

"In addition, the performance of the southwest monsoon amid concerns regarding occurrence of El Nino phenomenon and its impact on rural demand remains monitorable. The availability of semiconductor wafers to support desired production levels by OEMs will also continue to be key, and new capabilities likely only towards the end of CY2023,” he said.

Also Read: Toyota launches ‘Wheels on Web’; first ever online retail sales platform

Neha Mehlawat

Neha Mehlawat is an automotive journalist and industry analyst with 10+ years of experience covering cars, bikes, and mobility trends. She tracks the latest launches, technology upgrades, and policy changes in the auto sector, delivering sharp insights that help readers stay ahead in the fast-evolving world of automobiles.